For whom was it developed and how does It benefit you?

The Riester Rente started in 2002. It is mainly for people with high incomes and families with many children. Choosing between a tax rebate or a subsidy depends on which option is better and more helpful for you personally. The tax office will use this information when calculating your income tax each year. Anyone who pays into the state pension system can get a Riester Rente. People who are not eligible themselves, but are married to or registered as partners of someone who is eligible, can also get a Riester policy. They will get the full subsidy even if they only pay €60 per year in contributions. You need to submit a tax declaration every year to receive the full benefits. The monthly pension you receive is taxed according to your personal tax rate. As a pensioner in Germany, your tax rates are usually lower than when you were working.

How does it work, and what benefits do you get?

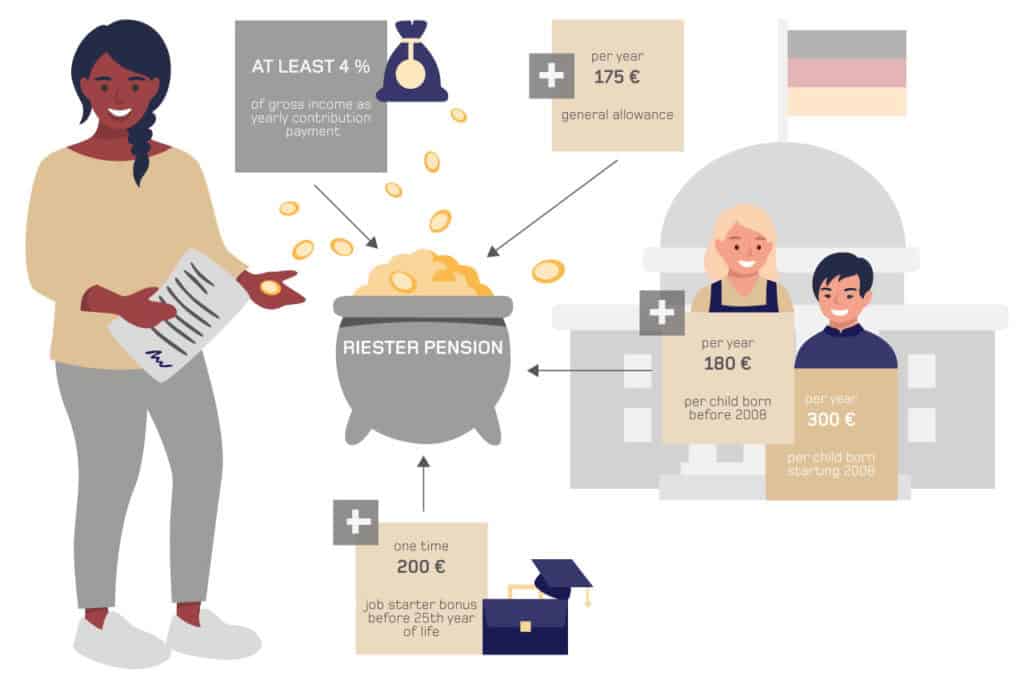

The government gives a yearly payment of €175 for each adult and €300 for each child (€185 for children born before 2008). In addition, if you are under 25 years old and start a Riester plan, you get a €200 bonus called the job starter bonus. You must pay into the state pension system to be eligible for the Riester Rente. To receive the full subsidy, you need to pay 4% of your gross income into the Riester plan, up to a maximum of €2,100 per year. The premiums you pay can be deducted from your taxes, so they are taxed later when you receive your pension payments. The advantage is that as a pensioner, you usually pay less tax because your income is lower than when you were working.

Options for capital allocation of your savings and inherent warranties

Most Riester Rente products invest your money in funds. This can give you higher returns, especially when interest rates are low. These products give you many fund options to choose from, including managed portfolios where experts handle the investments for you. An advantage of insurance-based products is that you can switch funds up to 12 times a year without any fees. Also, you do not have to pay capital gains tax on your profits until you start receiving your pension.

An extra benefit of all the premiums and subsidies is that the money you paid in is completely safe. This means that even if the fund loses money, you will not lose your pension. Finally, you cannot borrow money using your Riester pension savings as security. This means your savings are protected if you become insolvent (if you cannot pay your debts).

Payout and availability of contract balance

You can receive payments from your pension at the earliest when you are 63 years old. The pension will pay you money for your whole life. However, at the beginning of the pension payments, you can take out up to 30% of your savings as a one-time lump sum. Taking out the lump sum affects your taxes in the year when you withdraw the money. You can withdraw money from your savings at any time if you use it to buy a home where you will live. This option is called Wohnriester. The pension payments are guaranteed for the whole life of the person receiving them. If the person paying into the pension dies, the money saved so far will be transferred to the Riester policy of their partner. It is also possible to get the saved money as a lump sum, but then you will not receive any subsidies or tax benefits. If the person receiving the pension dies during the payment period, the pension will continue to be paid to the beneficiary for the agreed amount of time. This is called the guarantee period (Garantiezeit). The guaranteed payment period can last between 5 and 18 years. However, this can slightly reduce the amount of pension you receive each month. You can also receive the remaining money as a lump sum, but then you will not get any subsidies or tax benefits.

If the person dies, only their spouse (or registered partner) or their children can receive the benefits. The children can receive benefits only until they finish their first education, or up to the age of 25 at the latest. If the policyholder leaves Germany, their Riester pension will no longer receive contributions. The remaining balance will still stay active for the policyholder because their investment in the funds will continue. The Riester pension should only be used by people who plan to retire within the European Union (EU). If this is not the case, you will lose the subsidies and tax benefits.