For whom was it developed and how does It benefit you?

The Riester Rente was introduced in 2002 and targets particularly high-income earners and also large families. Whether one chooses the tax rebate or the subsidy depends on what suits and benefits the individual the most. This will be used by the tax office in their yearly income tax calculations. Anyone paying into the state pension scheme is entitled to a Riester Rente. Those who are not entitled to this, but are married to or registered as a partner of someone who is, are also eligible for a Riester policy. They will receive the full subsidy while paying only €60/year in contributions. It is necessary to submit a tax declaration every year in order to receive full benefits. The monthly pension received is taxed at the pensioners’ personal tax rate. As a pensioner in Germany, you usually have lower tax rates in comparison to the tax rates while employed.

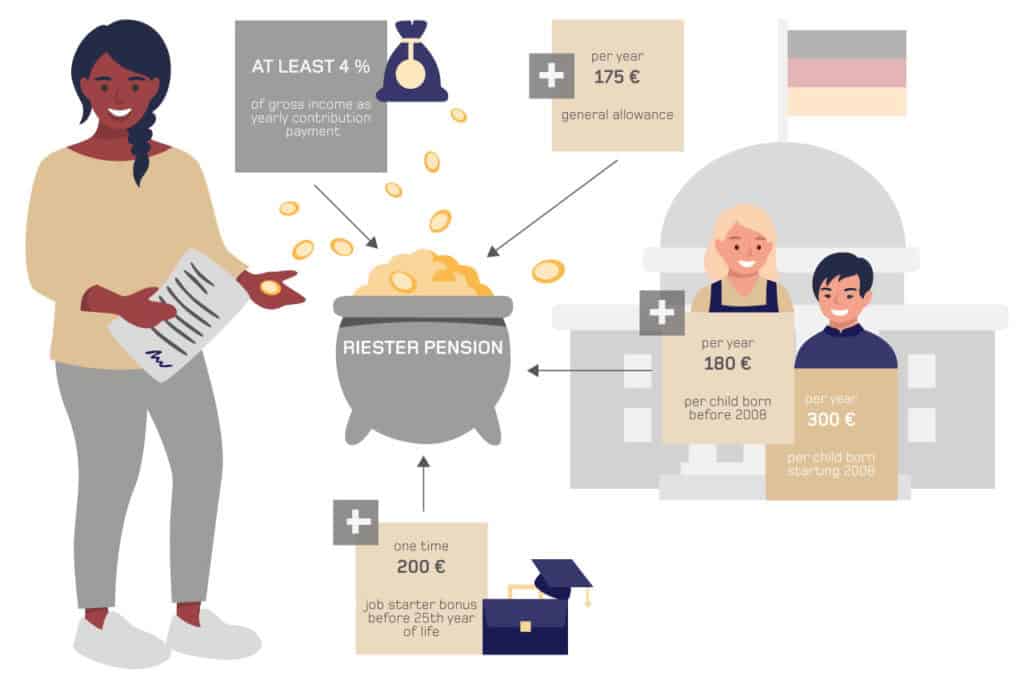

How does it work and what have you got to benefit?

The government pays a yearly subsidy of €175 per person and €300 for each child (€185 for children born before 2008). Moreover, a €200 job starter bonus is offered if you are less than 25 years of age and obtain a Riester. It is necessary to be paying contributions into the statutory pension scheme in order to be eligible for the Riester Rente. In order to get the full subsidy, you would need to pay 4% of your gross earnings into the scheme up to a maximum of €2,100/year. The premiums can be offset against tax and are therefore taxed when paid out. The advantage is that taxes in such cases are normally much lower as a pensioner, simply because the income is not so high.

Options for capital allocation of your savings and inherent warranties

Most Riester Rente products are funds-based investments, offering a higher return in the current low interest rate situation. The products themselves offer a wide range of funds to choose from, including managed portfolios. The advantage is that insurance-based products have is that you can switch funds up to 12 times a year, free of charge. Moreover, there is no capital gain taxes to be paid on the profits until the pension is withdrawn.

An added bonus for all the premiums and subsidies is that what they paid in is 100% guaranteed, meaning that even if the fund loses money, you will not lose your pension. Finally, capital cannot be borrowed against a Riester-Rente, which means it is protected from insolvency.

Payout and availability of contract balance

The earliest pay out opportunity is at age 63. It will pay out as a lifelong pension, but you can withdraw up to 30% of savings as a one-time capital payment at the start of the pension draw-down phase. The capitalization affects taxes in the year in which it is withdrawn. It is possible at any time to withdraw capital if it is to finance a property which will be occupied by the Riester Rente policyholder known as Wohnriester. The pension is guaranteed for the rest of the beneficiary’s life. In case of death during the paying-in phase, the amassed amount will be paid into the Riester policy of the partner of the deceased. It is also possible to receive the amassed capital, but without subsidies and tax benefits. In case of death in the time of the pension withdrawal, the pension will be paid out to the beneficiary for the arranged amount of time (Garantiezeit). The guaranteed pay out time can vary between 5 and 18 years. It does, however, have a small effect on the amount of pension that can be withdrawn per month. It is also possible to receive the remaining capital, without subsidies and tax benefits.

In the case of death, only the spouse (or registered partner) or the children until they have finished their first education (max. up to the age of 25) may be the beneficiaries of the deceased. Should the policyholder leave Germany, his Riester Rente policy will be set to non- contributory. The balance will still work for the policyholder as his investment in funds continues. The Riester Rente should only be used by people planning on retiring in the EU. If this is not the case, then the subsidies and tax benefits will be lost.