Deutsche Rente

In Germany, more than 30 million employees rely on the state pension as their main source of income after retirement. However, because the population is getting older and fewer young people are working, the number of pensions paid will decrease in the coming years. This means fewer employers will be able to pay for pensions. To keep your standard of living when you are older, it is very important to plan for a private pension. This extra planning helps protect you from becoming poor in old age.

Basic pension coverage often has gaps that are expected or likely to happen.

The German pension insurance (called DRV) was created in 1891 by Chancellor Bismarck. All employees must pay into this system. You can start receiving a normal pension at age 67. Early retirement is possible from age 65 but only in certain cases and usually means your pension is reduced by about 10%. Self-employed people can choose to join the system voluntarily. Some professionals like doctors or lawyers join special pension funds called Versorgungswerke instead of the DRV. Public servants get their pension from a different system called Beamtenversorgung, which is paid by the state, not the DRV.

It is crucial to mention that in order to be eligible for a lifelong pension, one must have paid a percentage for this for at least five years (>60 months). If you have worked in Germany for less than 60 months, on returning to a non-European country, you can request your share of contribution back up to two years after leaving Germany. Should you require such a service, we are here to assist you with our expertise so that this could be done correctly and securely. The contribution rate is currently 18.6%, half of which is to be paid by the employee and the other half by the employer. The billing and bank transfers are automatically carried out by the employer. No account – no interest rate – no capital formation. The DRV works by a ‘pay-as-you-go’ system known as Umlageverfahren. Also known as an intergenerational contract, working-generation pension contributions are directly used to finance the current pensions of the elderly; first in – first out. The DRV supposedly mentions a “pension account”, but in actual fact, this account does not contain any capital that is personally allocated to the insured person. Through FIFO, it is also not possible to create any capital that could bear interest.

Demographic problems and the pension level

The DRV’s ‘pay-as-you-go’ system depends on how many people pay into it and how much they earn. In the last 30 years, pensions in Germany have been reduced because many people lost jobs and stopped paying into the system. The problem will get worse as the last large group of babies born after World War II retire starting around 2025. For 50 years, birth rates have been low. On average, each retired couple has only 1.4 children to support their pensions. To handle this, the DRV uses a mixed approach: it raises the contributions people pay and lowers the pensions they receive. Because of these changes, the net pension level (which compares the pension amount to the last income before retirement) has decreased.

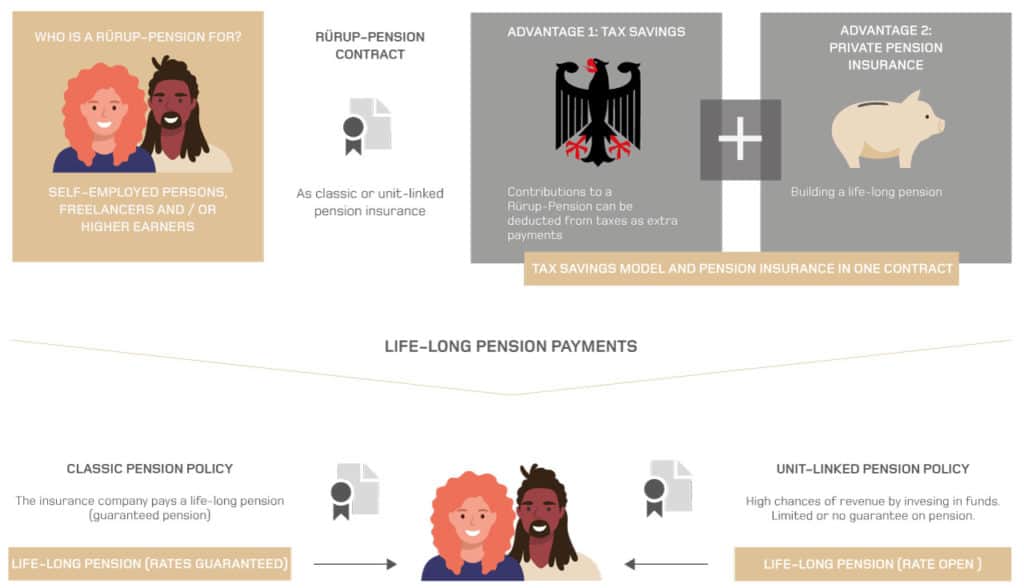

Basis Rente

As certified advisors who specialize in helping expats, we offer a special service. We guide our clients to understand and use three important allies for a good retirement: the power of compound interest (earning interest on your interest), the German state pension system, and our expert advice.

For whom is this targeted?

The Basis Rente was introduced in 2005 for self-employed people and those with high incomes. You can pay up to €25,787 per year if you are single, or up to €51,574 if you are married. Starting in 2025, these payments can be fully deducted from your taxes. You can choose to pay small monthly amounts and then pay a larger sum at the end of the year, after seeing your total income, to reduce your taxes. The Basis Rente gives you a pension for your whole life. You can start withdrawing this pension from age 63 at the earliest.

There are limits on how much you can pay into certain pension plans to get tax benefits. The government supports these plans by allowing you to deduct your payments from your taxes, up to these limits.

In 2004, the average pensioner received about 50% of their final income as a pension. By 2030, this amount is expected to drop to around 43%. One main reason is a tax reform called the age-related income act. Since 2005, you can deduct 60% of your pension contributions from your taxes, with this percentage increasing every year until it reaches 100% in 2025. However, the pension payments you receive will be taxed more over time, reaching 100% taxation from 2040. For example, a pensioner who retired in 2005 paid tax on 50% of their pension, while in 2025, an employee’s contributions to the pension system will be fully tax-free.

The Rürup Rente is named after its founder. You can combine payments made to the state pension system and the Basis Rente, up to a total of €25,787 per year if you are single, or €51,574 per year if you are a couple (married or in a registered partnership). For example, a single person earning €85,200 in 2021 pays a maximum of €14,954 into the state pension system, including employer contributions. This means they still have €9,350 per year (or about €779 per month) that they can save for retirement using the Basis Rente. From these savings, they can get up to a 45% tax return each year on their tax declaration.

Taxation of savings and pensions

In 2021, you can deduct 92% of your pension contributions from your taxes. This percentage will increase by 2% every year until 2025, when it will reach 100%. This increase happens automatically, no matter when you started your pension plan.

You can pay small amounts every month and then add a larger payment at the end of the year to make the most of the tax benefits. When you receive your monthly pension, it will be taxed according to your personal tax rate. Tax rules for pensioners in Germany are different from the rules during working years.

Multiple allocation methods for your savings

Most Basis Rente products invest your money in funds. These products offer many fund options, including actively managed ones where experts choose the investments. A benefit of these insurance-based products is that you can switch funds up to 12 times a year without extra fees. You also do not have to pay capital gains tax when switching, unlike normal ETF savings plans.

Useful features for worst case scenarios

You cannot borrow money from a Basis Rente, and its value cannot be taken away by others. It is protected if you become unemployed or insolvent (unable to pay debts). The pension is guaranteed to pay you for the rest of your life. You can start receiving payments at age 62 through a German bank account. If you die while still paying into the plan, the saved amount will be paid to your legal beneficiaries, like a partner or heirs. The guaranteed payout period can be between 5 and 18 years, which means the monthly pension amount might be a bit different depending on this choice.

If you decide to leave Germany, you can stop making payments to your Basis Rente policy, but it will stay active. The money already invested will keep growing in the funds. When it is time to receive your pension, it will be paid to you in your new country of residence.