A private pension plan is one of the most popular ways to save for retirement in Germany because it is flexible.

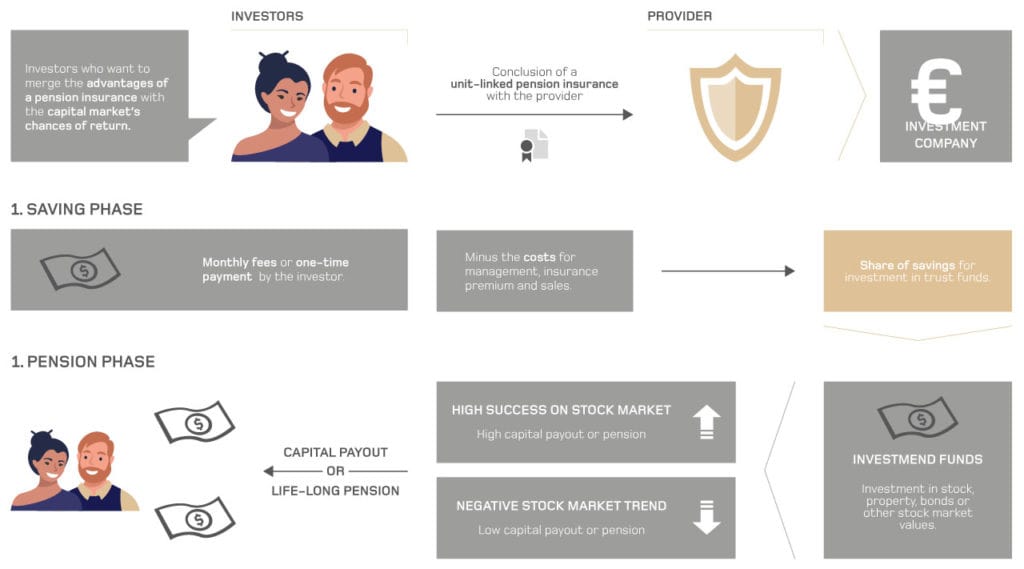

Almost every bank and insurance company offers a flexible private pension plan called Private Rentenversicherung. The bank or insurance company manages this plan for you. However, you have full control over how your money is invested.

Who is it for, and what are the basic rules?

The Private Rente is designed for every citizen to use and benefit from. It is especially attractive and a good choice for expats because it is flexible. You can keep adding money to this retirement account no matter where you live. This is important and makes moving away from Germany easier to manage. You get tax benefits when the policy reaches pension age. From that time, it is your choice to use it as a backup plan along with your other pensions. When the policy reaches maturity, you can choose to get all the money at once, part of it as a lump sum, or receive regular payments for your whole life.

Payout options and capital allocation methods

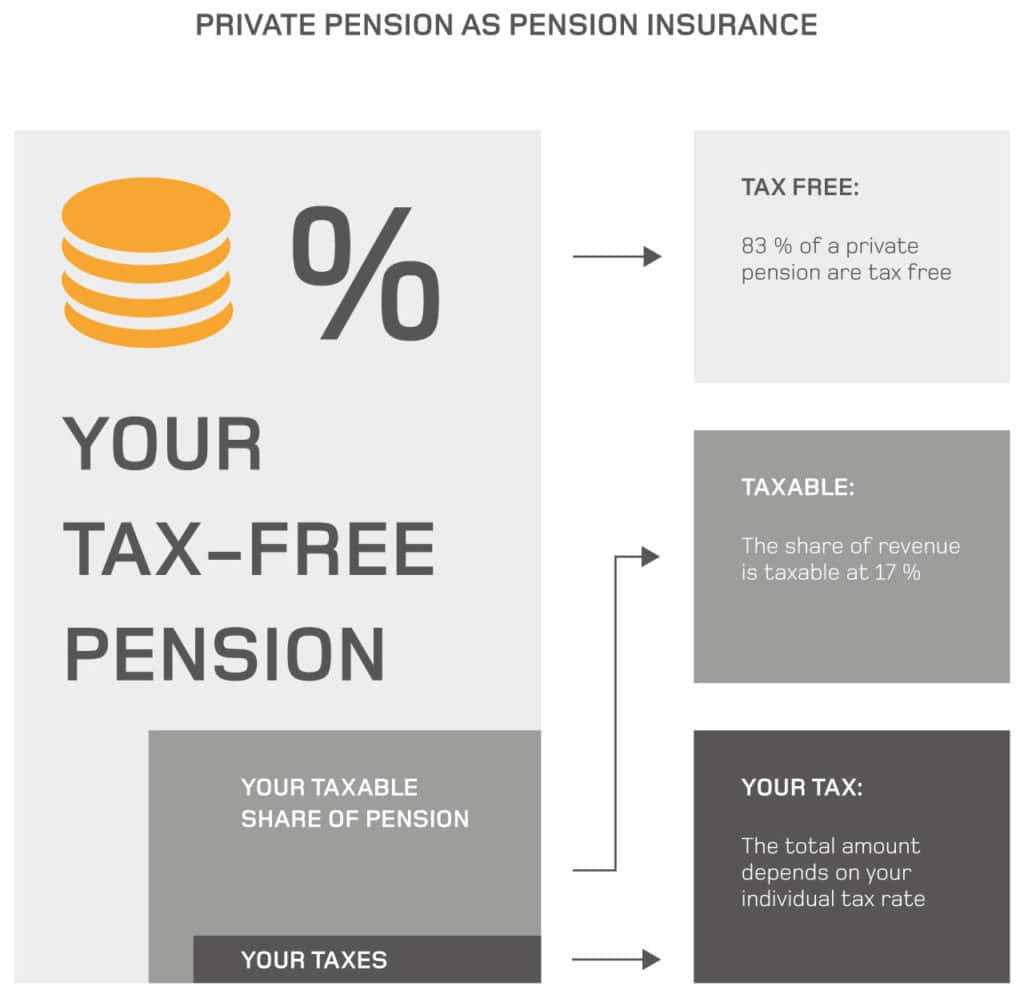

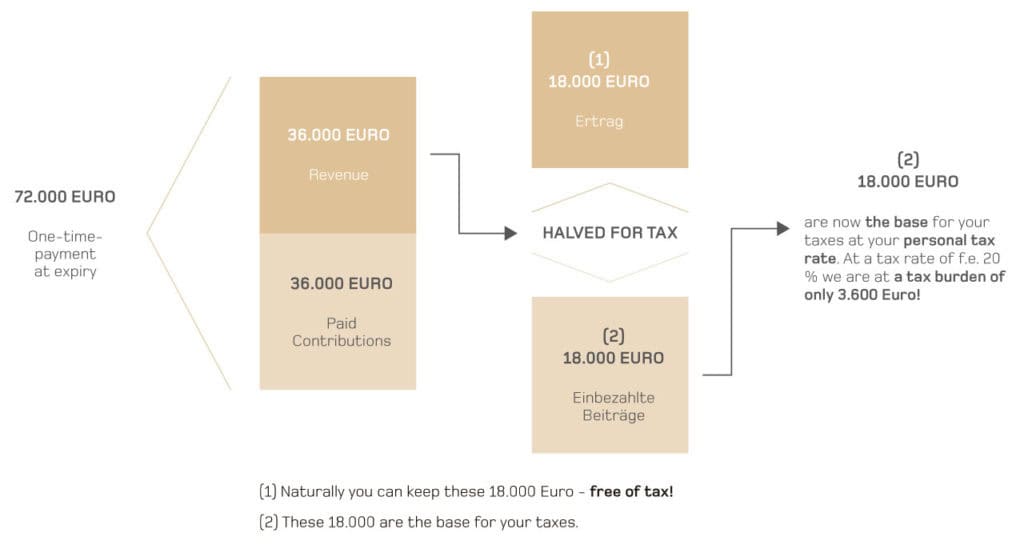

You can start receiving your pension payments right away or choose to start at a later time. Most of these pension plans invest your money in funds (groups of investments). These pension plans offer many types of funds to choose from, including ETFs (Exchange-Traded Funds) and actively managed portfolios (where experts pick the investments). The benefit of insurance pension plans is that you can change your investment funds at least 12 times a year without paying any fees or taxes on the profits. If you feel that investing in financial markets is too risky, some insurance companies offer a traditional plan with a guaranteed interest rate. Right now, this rate is 0.9% per year. Additionally, because insurance companies invest your money, they share some extra profits with you. This is called Überschusse (profit participation). Right now, the total return is at least 2.25% per year, but this can be a little different depending on the company. You can borrow money using your Private Rente as security. However, this borrowed money can be taken away and counted when calculating your unemployment benefits. At the end of the saving phase, you can choose to get your money as a lump sum, a lifelong pension, or a combination of both. If the contract lasts at least 12 years and you withdraw the money at the earliest age of 62, there are two different ways the money can be taxed. If you choose to take the money as a lump sum, you will pay tax on 50% of the profits at your personal tax rate. If you choose a lifelong pension, only the profit part of the payments (called Ertragsanteil) is taxed. The Ertragsanteil is a fixed percentage that depends on the age when you start receiving the pension. For example, at age 62 it is 21%, at 63 it is 20%, at 64 it is 19%, at 65 to 66 it is 18%, and at 67 it is 17%. If you start receiving a pension of €1,000 at age 65, you will only pay tax on €180 of that amount, using your personal tax rate. If the conditions mentioned above are not met, the full amount will be taxed with the withholding tax called Abgeltungssteuer. This tax rate is currently 25%. The pension payments are guaranteed for the whole life of the person receiving them.

Flexibility features in the Private Rente

You can withdraw part of your Private Rente savings at any time. You can also take a loan using the money you have saved so far as security. Usually, each withdrawal must be at least €1,000, and you must keep at least €2,500 in the account after the withdrawal.

You can cancel the contract at any time. If you do, the money saved in your account will be paid out to you. It is not a good idea to cancel the contract during the first few years. This is because the costs charged during the early years would reduce the amount of money you get back. You can also add an occupational disability insurance to your pension plan. This insurance helps if you cannot work due to illness or injury. If the person paying into the pension dies, the saved money will be paid to the person they named as beneficiary. If the person receiving the pension dies during the payment phase, the money will be paid to the named beneficiary for the agreed period of time. This is called the guarantee period (Garantiezeit). The guaranteed payout period can last between 5 and 18 years. However, this slightly reduces the amount of pension you can receive each month. If the policyholder leaves Germany, the policy can either continue or be set to stop receiving contributions. The remaining balance will still be active for the policyholder because the investment in the funds will continue. You will receive the lump sum payment or retirement pension whether you live in Germany or another country.