Betriebliche Altersvorsorge

The BAV is a workplace pension plan that is connected to your job. The BAV offers many benefits and ways to save money safely for your retirement. According to the Pension Strengthening Act (Rentenverstärkungsgesetz), every employee should be given the chance to set up an additional pension.

Combining employer and governmental support in your pension

All employees in a company have the right to join a pension scheme where they can add money themselves, not only their employer. If you, as an expat business owner, do not have a pension scheme yet, our experts can advise you free of charge at your workplace about the options available.

If you hire skilled expats in your company, we can also offer a general seminar or individual sessions to teach them about personal finances. These sessions will be designed to meet their specific needs.

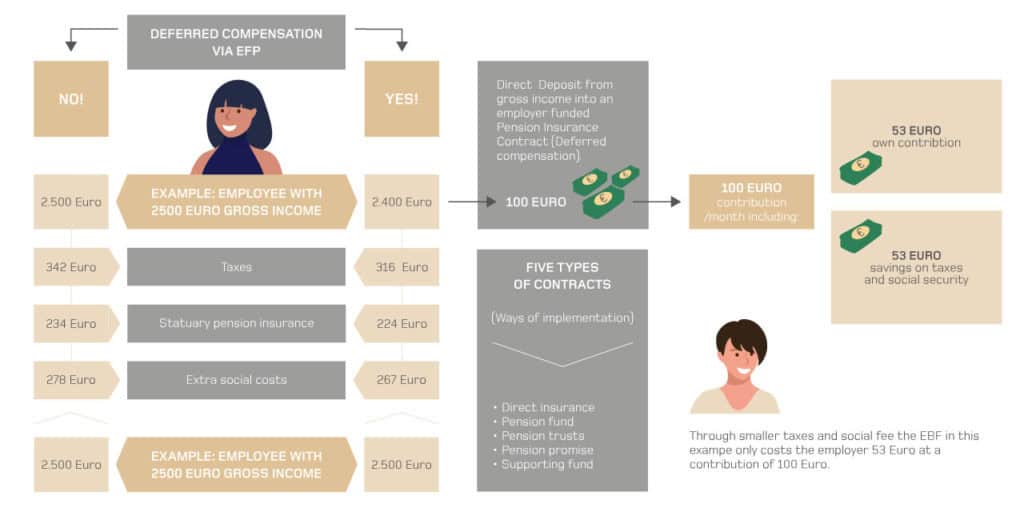

Employees can ask their employer to not pay part of their salary as money. Instead, this part can be saved in a company pension plan. This is called ‘deferred compensation’. If you choose a BAV pension plan, your employer must by law take up to 8% of your salary before taxes (up to a maximum of €6,240 per year) and use this money to pay into your BAV directly. Alternatively, 4% of your salary can be taken before you pay taxes and social security contributions.

Who is eligible for BAV?

Company pension schemes are available to employees. This includes salaried employees, wage earners, trainees, managers who own part or all of a company (GmbH), and members of the board of directors of a corporation. Additionally, company pension schemes can be offered to external workers if they work only for one company.

Designing options and flexible forms

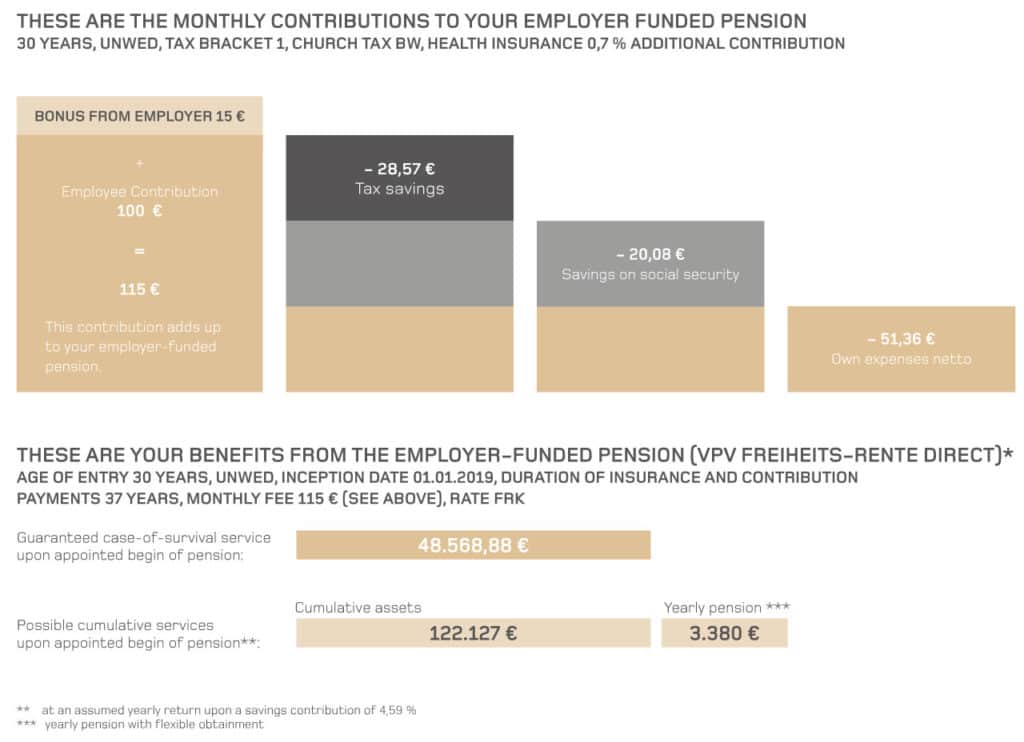

Of course, you can take your company pension savings with you if you change your employer. Occupational pension schemes work in the same way as private pension insurance plans. Your employer can decide which insurance company is used for the BAV pension plan. As the employer, you will also save half of the social security contributions for your employees. The employee must also pay a minimum contribution to the scheme. This is 15% of the amount saved. The money saved can be paid to you in different ways. You can receive a lifelong pension, where you get a fixed amount every month for the rest of your life based on your saved money. You can get all the saved money at once as a full lump sum. Or you can take part of the money, usually about 30%, as a lump sum, and get the rest later as a lifelong pension.

You will have to pay taxes and social security contributions when you receive the pension payments, either during retirement or whenever you get the money. If you signed a BAV contract after 2012, you can start receiving benefits earliest at the age of 62. However, you usually start receiving these benefits when you first claim your full German state pension. It is important to know that if you pay less social security, you are also paying less into the German state pension. This means your state pension may be lower later. This means that the pension you get from the German pension insurance (DRV) when you retire will be a little lower.